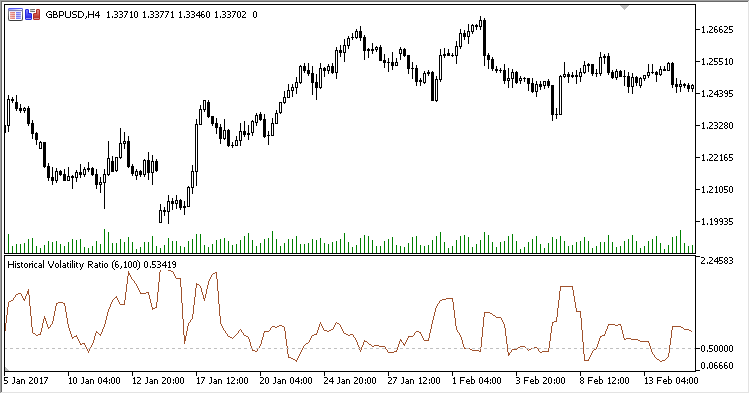

Oscillator Historical Volatility Ratio is a volatility indicator based on the "yesterday" / "today" price ratio

It has four configurable parameters:

- First deviation period - first standard deviation calculation period

- Second deviation period - second standard deviation calculation period

- Applied price - calculation price

- Threshold - "low" volatility threshold

Calculation:

HVR = StdDev1 / StdDev2

where:

StdDev1(ST) - standard deviation with the First deviation period

StdDev2(ST) - standard deviation with the Second deviation period

ST = LOG(Price/PrevPrice)